Talosnation

Imagine a world where banks effortlessly maximize profits while minimizing risks. The key lies in the efficiency of their lending processes. Lending is not just a cornerstone of banks' income; it's a strategic imperative. The smoother the process, the healthier their margins. Traditionally, the lending process comprises five essential steps:

- Loan Origination

- Credit Appraisal

- Loan Processing

- Loan Servicing

- Default Management

In this series of newsletters, we will delve into each of these steps, examining their roles and how Robotic Process Automation (RPA) can revolutionize efficiency.

Today, we kick off with Loan Origination, the pivotal first step that defines the success of the entire lending journey. In the complex world of banking, loan origination is a critical process that ensures both retail and commercial customers receive the financial support they need. Whether it's an individual seeking a personal loan or a business looking for commercial financing, the loan origination process is designed to be thorough and precise. Here’s a detailed look at the loan origination workflow for both retail and commercial loans

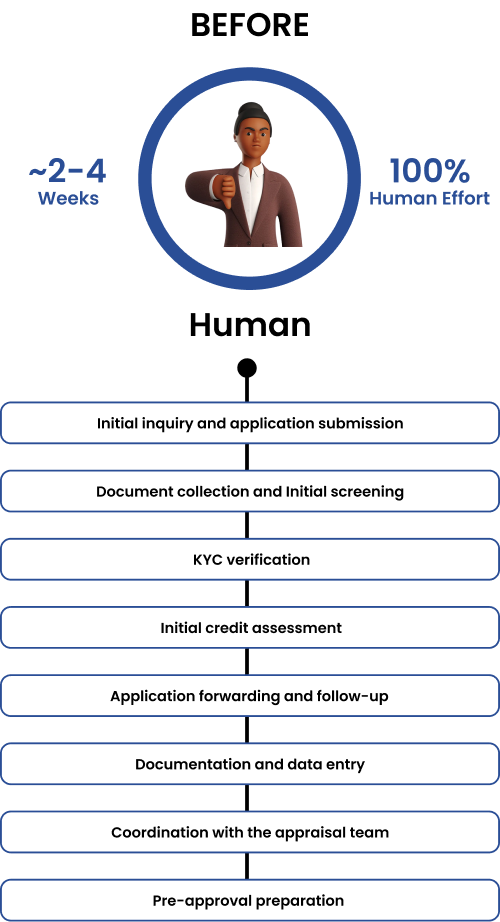

1. Initial inquiry and application submission

The journey begins with an initial inquiry. For a retail customer, this might be an individual walking into a branch or visiting the bank’s website, seeking information about personal loan options. For a commercial customer, it could be a business representative looking for financing to expand operations. During this stage, bank employees play a crucial role in providing detailed information about the available loan products, eligibility criteria, interest rates, and required documentation.

Once the potential borrower has gathered enough information, they proceed to fill out a loan application form. This form can be provided physically or digitally, depending on the bank’s capabilities. Bank employees often assist in completing this form to ensure all necessary fields are accurately filled out, setting the stage for a smooth application process.

2. Document collection and Initial screening

With the application form completed, the next step involves collecting all necessary documents. For retail loans, this includes identity proof, address proof, income proof, bank statements, and employment details. For commercial loans, the documentation is more extensive, requiring financial statements, a business plan, collateral details, and identity proof of key stakeholders.

Bank employees then perform an initial screening to verify the completeness of the application and ensure all required documents are submitted. They also conduct a preliminary eligibility check based on basic criteria such as minimum income, age, and employment status for retail loans, and minimum revenue, business age, and industry for commercial loans. This initial screening helps identify any immediate issues that could prevent the application from moving forward.

3. KYC verification

KYC verification is an essential part of the loan origination process, crucial for both external applicants and existing bank customers. For retail loans, bank employees verify the borrower’s identity and address using documents such as Aadhar, PAN, or passport. In the case of commercial loans, verification extends to the business and its key stakeholders. Additional background checks may also be conducted to ensure the borrower's credibility, maintaining the accuracy and currency of the bank's KYC records.

4. Initial credit assessment

The initial credit assessment is where the bank begins to evaluate the borrower’s financial health. A critical part of this assessment is obtaining a credit bureau report, which provides insight into the borrower’s credit history. For retail customers, this includes reviewing past loans, repayment behaviour, and existing liabilities. For commercial customers, the focus is on the credit history of the business and its key stakeholders.

Bank employees evaluate the credit score and discuss any concerns or red flags with the borrower. This evaluation helps the bank understand the borrower’s creditworthiness and ability to repay the loan, laying the groundwork for the detailed credit appraisal that follows.

5. Application forwarding and follow-up

With the initial assessment complete, bank employees compile all the collected information into an initial report. This report includes the completed application form, collected documents, and findings from the initial credit assessment. The application and report are then forwarded to the credit appraisal team for detailed analysis and assessment.

Throughout this process, it’s crucial to keep the borrower informed about the status of their application. Regular communication ensures that any additional information or documents required are promptly provided, and any questions or concerns from the borrower are addressed, fostering a transparent and efficient loan origination process.

6. Documentation and Data entry

As part of the loan origination process, accurate documentation and data entry are essential. Bank employees enter all relevant borrower information and application details into the bank’s loan origination system. They also scan and upload all collected documents for record-keeping and further processing. This step ensures that all information is centralized and accessible for subsequent stages of the loan approval process.

7. Coordination with the appraisal team

Effective coordination with the credit appraisal team is vital for a successful loan origination process. Bank employees provide any additional information or clarification needed during the detailed appraisal process. They monitor the progress of the appraisal and keep the borrower updated, ensuring that the application moves forward without unnecessary delays.

8. Pre-approval preparation

Finally, as the loan application nears approval, bank employees prepare for the final stages. They compile all documents and information required for the final approval process, conducting a final review to ensure completeness and accuracy. This meticulous preparation helps prevent any last-minute issues, paving the way for a smooth and successful loan approval.

Tackling Loan Origination Challenges with AI and RPA

Now that we've uncovered how loans get started, let's explore the bumps along the way. See how we can transform this process with advanced RPA and AI technologies, paving the way for smoother, more efficient operations and exciting innovations.

Getting loans started can be tough, with slow paperwork, mistakes, and rules to follow. Let's find out how new tech like RPA and AI can make things faster and better, giving us more time to focus on what really matters.

1. Initial inquiry and application submission

Problem!

During initial inquiries, having customer service agents handle face-to-face interactions often results in higher customer satisfaction. However, these agents might not be familiar with all the intricate details of the bank's lending rules and guidelines, and they cannot provide support 24/7. If applications are not properly verified at this initial stage, it can lead to time delays for both the customers and the bank, resulting in increased operating expenses and lower customer satisfaction.

How Our RPA Can Help?

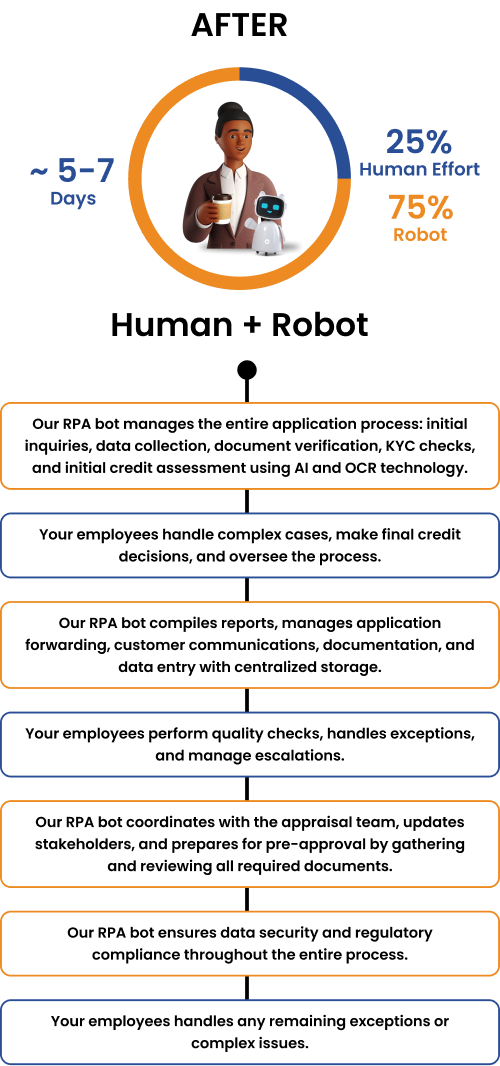

An RPA bot can provide 24/7 support for online customer inquiries, enhancing customer satisfaction. It can gather client information, determine the type of loan they seek, and forward this data to the appropriate department or person. Additionally, the RPA bot can assist with data collection and verification by using OCR technology to process scanned copies of physical application forms or by directly handling online forms. This automation saves time for customer service agents and ensures accurate data entry in the bank's system.

2. Document collection and Initial screening

Problem!

Once we start collecting the documents, it is necessary to make sure that all the necessary documents are collected and to be verified that it has the correct information, and nothing is missing form them. As both types of loans requires two different sets of documents, it is necessary to make sure there is a check list of documents required for each type of loan is created so that it is easier for the agent too and nothing goes missing. But to verify and validate all the necessary information are there in those documents and nothing’s missing would be a whole other ball game. It is physically impossible for an agent to do this manually. But, if this is done at this stage and the application passes, the bank can be sure that there would be no other issues which would occur from the incomplete application in the later stages of the process.

How can our RPA bot help?

RPA bots can handle all of this effortlessly, saving the bank and agents from many headaches, cups of coffee, and wasted time. They can quickly review the list of required documents and check them against a predefined checklist. Using OCR technology, RPA bots can also validate the documents to ensure all necessary information is present. They can process all applications in a fraction of the time it would take a human. If anything is missing, the bot can automatically notify both the agent and the customer. This significantly reduces the time needed for the application process. Additionally, RPA bots can enter data directly into the system, making the process more efficient and less linear.

3. KYC verification

Problem!

KYC verification is a crucial step in the loan origination process but can be extremely time-consuming for the bank and employees if there's no automated process in place.

How can our RPA bot help?

Our RPA bot can streamline this process by accessing information from online portals to verify the customer and perform background checks. In the case of Indian banks, while the agent verifies the customer using eKYC methods, the RPA bot can handle the data retrieval and verification, saving valuable time and reducing manual effort.

4. Initial credit assessment

Problem!

The initial credit assessment for retail loans is straightforward, involving a review of credit history and past loans. However, for commercial loans, the process is far more complex, involving large amounts of data and documents, and numerous potential red flags. Information fatigue can lead to key details being missed by employees, resulting in potentially disastrous outcomes.

How can our RPA bot help?

For both retail and commercial loans, our RPA bot can efficiently verify the creditworthiness of clients, simplifying the underwriter's job in later stages. Powered by specialized AI that can be tailored to each bank's processes, the RPA bot can perform these tasks at lightning speed and with greater accuracy than a human. Incorporating AI into this step can be a game changer, significantly reducing errors and improving overall efficiency.

5. Application forwarding and follow-up

Problem!

While employees can handle tasks effectively, human complacency can lead to missed deadlines and errors, particularly when compiling information into initial reports and application forms for credit assessments. Missing regular communication with customers can lead to dissatisfaction and concerns about transparency and progress updates.

How can our RPA bot help?

Our RPA bot excels in compiling and entering verified information into the required fields swiftly and accurately. By automating these tasks, it minimizes errors and substantially reduces the time needed to complete this process. This ensures a more efficient and reliable workflow, free from the inconsistencies that can arise from human oversight and complacency. It can also automate communication processes, ensuring timely updates and notifications to customers throughout the loan application journey. By maintaining regular and consistent communication, it enhances customer satisfaction and builds trust, ultimately improving the overall customer experience.

6. Documentation and Data entry

Problem!

Human errors in data entry often necessitate automation and automated applications.

How can our RPA bot help?

Our RPA bot excels in data entry, surpassing human performance in speed and accuracy. It efficiently manages and retrieves all collected documents, ensuring centralized storage and easy accessibility for comprehensive record-keeping. This capability enhances efficiency and maintains meticulous organization, improving overall operational effectiveness effortlessly.

7. Coordination with the appraisal team

Problem!

Automatically updating all stakeholders on the application status and aiding the appraisal team with necessary information would streamline the entire process, ensuring efficiency and customer satisfaction. Human oversight may lead to lapses in reminding the coordination team, especially when managing multiple loan applications simultaneously.

How can our RPA bot help?

Our RPA bot excels in coordinating with multiple teams for various loan applications effortlessly. It can send reminders, update all stakeholders promptly, and ensure no deadlines are missed. This capability not only enhances operational efficiency but also maintains seamless communication across all stages of the loan appraisal process, keeping customers satisfied with timely updates.

8. Pre-approval preparation

Problem!

As loan applications approach approval, bank employees prepare for the final stages by gathering all required documents and information. However, human errors can occur during this critical phase, potentially leading to inaccuracies and incomplete submissions.

How can our RPA bot help?

Our RPA bot could also excel in meticulously compiling all necessary documents and information with utmost precision. It conducts thorough reviews to guarantee completeness and accuracy, minimizing the risk of last-minute complications. This streamlined approach ensures a smooth and successful loan approval process, enhancing overall efficiency and customer satisfaction.

Additional benefits of RPA:

Data security and regulatory compliance are major concerns in the loan origination process. With RPA, we can create automated workflows that follow all compliance rules. RPA can easily work with older bank software because it doesn't rely only on APIs.

With these advancements, our RPA bot automates up to 75% of the loan origination process, allowing your employees to dedicate more time to personalized customer service and strategic decision-making. Whether it's streamlining initial inquiries, ensuring meticulous document verification, or expediting KYC processes, RPA optimizes efficiency across the board. By enhancing compliance and operational effectiveness, RPA not only meets regulatory standards but also elevates overall customer satisfaction.

Embrace the future of banking with RPA—a transformative force that drives efficiency, reliability, and unparalleled customer experiences in loan origination and beyond. Contact TalosNation today to discuss how RPA can address your specific challenges or any other needs you may have.